I’ve always been a fan of the Credit Union formerly known as Boeing Employees’ Credit Union. I joined all the way back in 1990, when you actually needed to have worked there, or be related to someone who had worked there. I was technically neither, although one of my best friends had just started there and he was (like a) brother to me. Later I ratified my membership when I got married; my wife had enjoyed a six month stint at the Company just after her college graduation.

But now, you just have to fog a mirror…there is no exclusivity to membership. In fact, they have formally truncated their name to “BECU,” I’m sure in order to make it clear that you don’t have to work for “Boeing’s” to be a member.

Why join? Here are a few unique and compelling reasons which I discovered during a recent visit to their neighborhood banking center, in the Shoreline Safeway (on 15th NE):

- You don’t have to drive to Tukwila to make a deposit. Time was, you’d have to go to the sole location near Boeing Field to sign documents or transact business. Now there are little kiosks virtually everywhere — there’s a new one in Lake City, for example, on Lake City Way near the new Bartell’s;

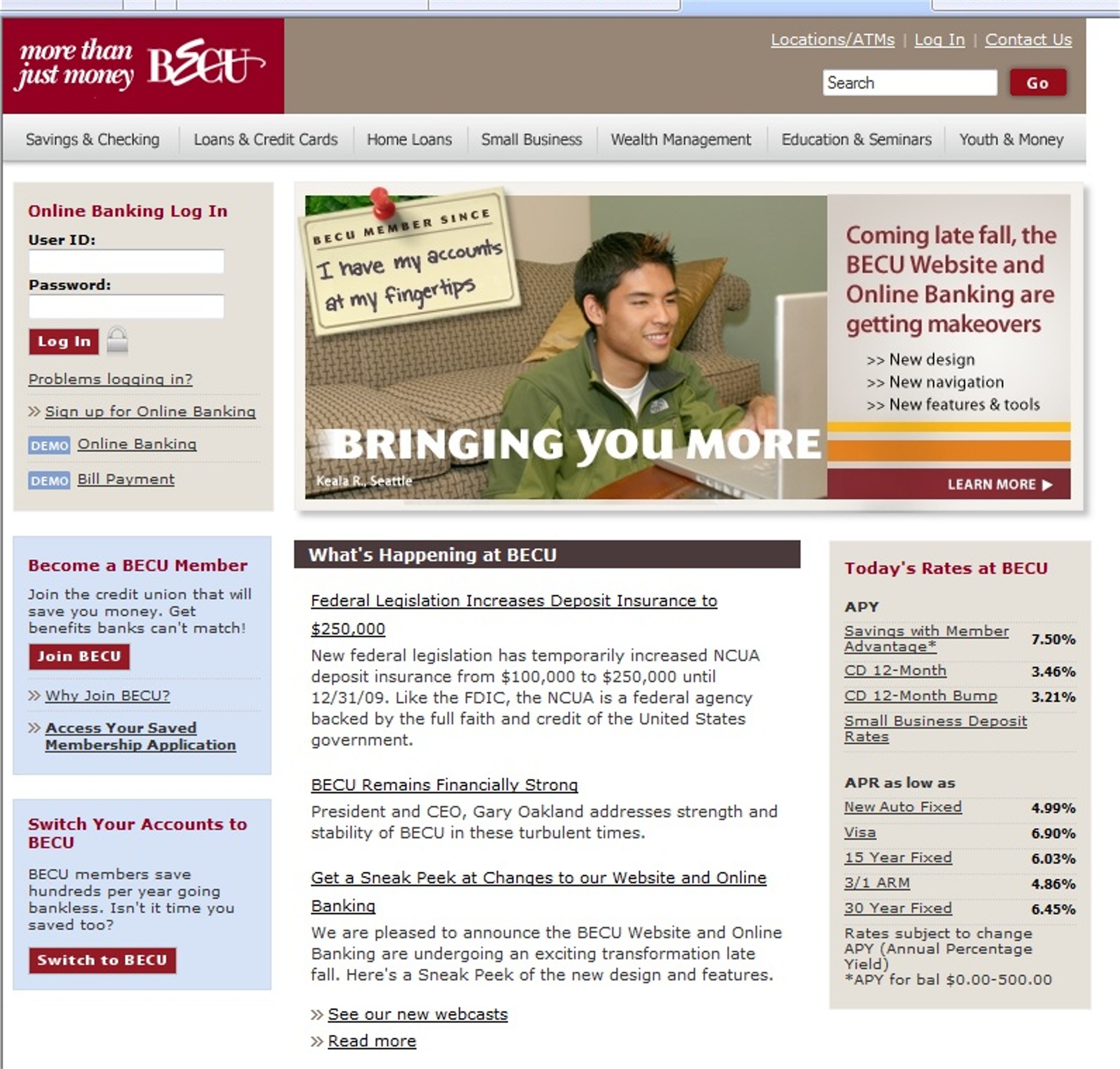

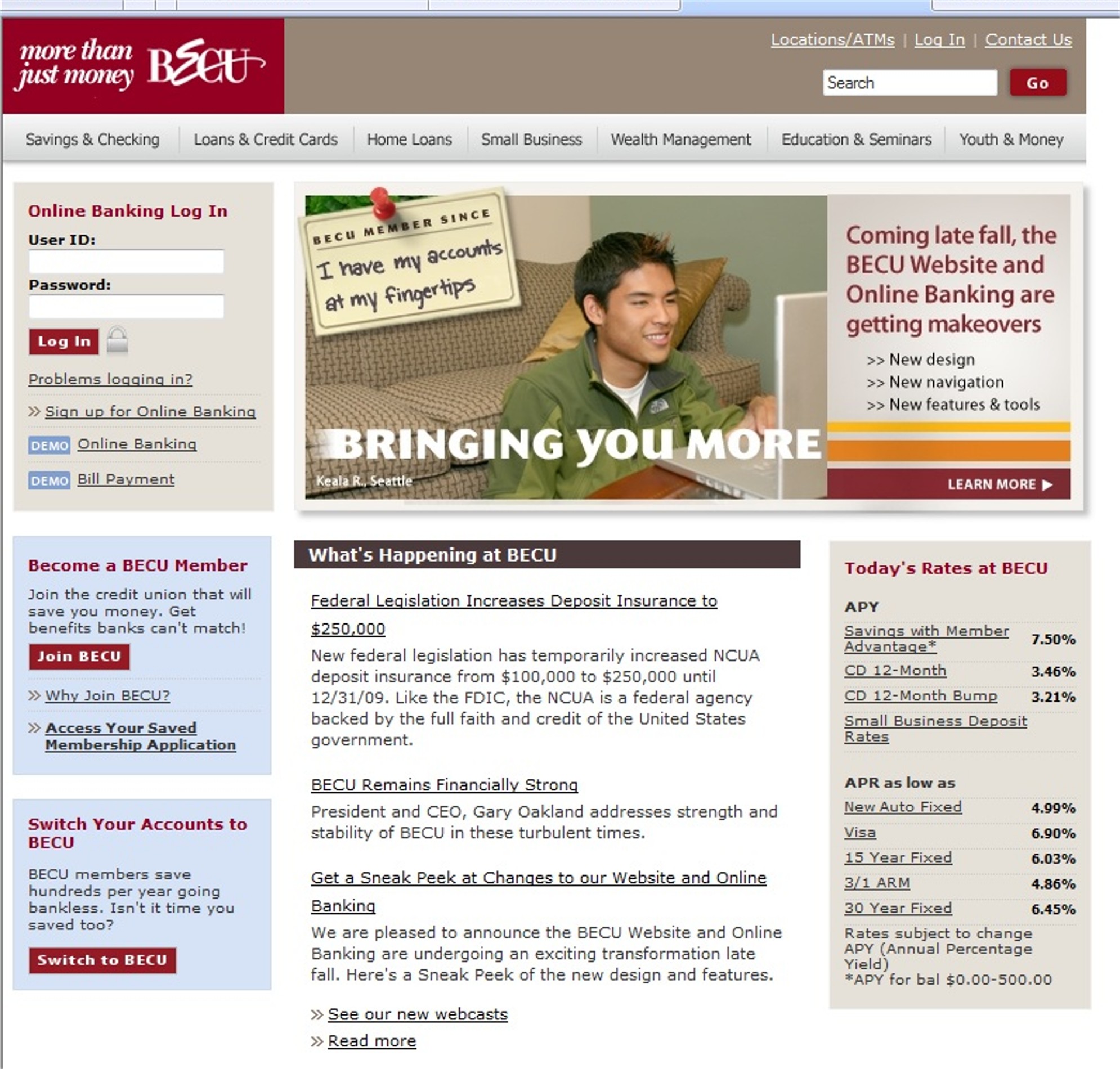

- 7.5% interest rate paid on the savings account. That’s right. 7.5%. Crazy. It’s a loss leader, and they cap it at $500 in deposits, but how fun will it be for my kids to take their $500 savings accounts out of WaMu (which we should probably do anyway) and actually learn how $37.50 in interest income is calculated;

- Consumer loans — there’s no place else. As a credit union, BECU is a non-profit. This means that they plow their profits into theoretically reduced rates for their borrowers. Plus they loan their own money — $11bn of it — on these loans. No funny money, CDS’s, CMO’s or any of those notorious acronyms here. If you need a car, boat, or other loan, this is the place. VISA’s too, although I won’t give up my Alaska Card from BoA.

- Best reason — HELOC’s. Home Equity Line of Credit. The rate is prime MINUS .75%. This is about 4.25% today, and if you advance on the line, you have the option of locking in a rate that is some margin higher than the floating rate. And it’s EASY to originate these — up to $250,000. Beyond that amount, there is more work for appraisals and verification of income, but up to $250k, it’s credit and equity checks (based on tax assessment, maybe a Zestimate?), and sign here. One week closing. I closed on my first BECU heloc in 1990 the day after I bought my second house, in Cedar Park. It reimbursed me for my entire down payment and paid for the remodel. Sounds like funny money, but turns out I was good for it :-). I don’t know if it’s THAT loose now, but it’s close. Even if you don’t need the cash now, set up this line of credit so it’s there as your rainy day fund. Be disciplined about not using it unnecessarily, of course. But the fact that BECU has money to lend, and is so easy to work with, is unique among banks these days. Try getting a new home equity line at BoA, Wells, or US Bank. Good luck with that.

- Also a great reason — community support. My wife is fundraiser for our kids’ PTA, and when I was at that banking center, I asked the manager if she had budget to support their literacy campaign. “Absolutely” was the answer. They have budget and love to pay back into the local communities.

For home mortgages, first mortgages, there’s not great deal here compared with any other good lender. This is because they do actually resell these into the secondary market like everyone else (Fannie, Freddie), so the programs have to conform. But anything else, this is the first place to look.

{kind=link}

{kind=link}

{kind=link}